How to Choose Between High vs. Low-Deductible Health Plans-www.waukeshahealthinsurance.com-www.waukeshahealthinsurance.com

Your deductible is the amount of money you must pay out-of-pocket for covered healthcare services before your health insurance plan begins to pay. Once you meet your deductible, your insurance company starts covering a portion of your medical expenses, according to your plan’s co-insurance and co-pay structure.

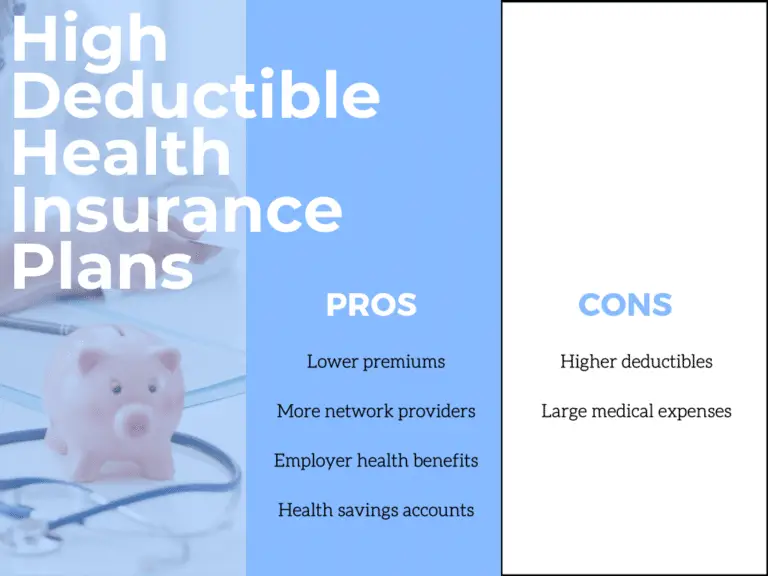

High-Deductible Health Plans (HDHPs):

HDHPs require you to pay a significantly higher deductible before your insurance coverage kicks in. The upside is that they typically come with lower monthly premiums. This makes them attractive to individuals and families who are generally healthy, rarely require medical care, and prioritize saving money on monthly payments. However, if you anticipate needing significant medical care, an HDHP could leave you with substantial out-of-pocket costs.

Pros of HDHPs:

- Lower monthly premiums: This is the primary advantage. You’ll pay less each month for your insurance.

- Potential for tax advantages: If you have a Health Savings Account (HSA), contributions are tax-deductible, and the money grows tax-free. You can use the funds for qualified medical expenses, and any remaining balance rolls over year to year. www.waukeshahealthinsurance.com can provide more information on HSAs and their compatibility with HDHPs.

- Greater control over healthcare spending: The high deductible encourages you to be more mindful of your healthcare spending, potentially leading to more cost-conscious decisions.

Cons of HDHPs:

- High out-of-pocket costs: If you experience a serious illness or injury, you’ll be responsible for a substantial amount of money before your insurance starts to cover expenses.

- Risk of financial hardship: Unexpected medical bills can be financially devastating with a high deductible.

- Potential for delayed care: The high cost of care upfront might lead some individuals to delay necessary medical attention.

Low-Deductible Health Plans (LDHPs):

LDHPs have lower deductibles, meaning your insurance company will start covering your medical expenses sooner. This provides greater financial protection against unexpected medical bills. However, the trade-off is higher monthly premiums.

Pros of LDHPs:

- Lower out-of-pocket costs: You’ll pay less out-of-pocket for medical care, providing greater financial security.

- Peace of mind: Knowing that your insurance will cover a significant portion of your medical expenses can reduce stress and anxiety.

- Access to care: You’re less likely to delay necessary medical care due to cost concerns.

Cons of LDHPs:

- Higher monthly premiums: You’ll pay more each month for your insurance coverage.

- Less control over healthcare spending: The lower deductible might lead to less mindful spending on healthcare services.

Factors to Consider When Choosing:

Several factors should influence your decision between an HDHP and an LDHP:

- Your health status: If you are generally healthy and rarely need medical care, an HDHP might be a good option. However, if you have pre-existing conditions or anticipate needing frequent medical care, an LDHP might be more suitable.

- Your financial situation: Consider your ability to handle a large out-of-pocket expense. If you have a limited financial buffer, an LDHP might offer better protection.

- Your age: Older individuals are more likely to require more medical care, making an LDHP a potentially better choice.

- Your family’s health history: If you have a family history of serious illnesses, an LDHP might be a wiser decision.

- Your risk tolerance: Are you comfortable taking on more financial risk in exchange for lower premiums?

Beyond Deductibles: Other Important Considerations:

While the deductible is a crucial factor, other aspects of your health insurance plan are equally important:

- Co-pays: This is the fixed amount you pay for each doctor’s visit or other service.

- Co-insurance: This is the percentage of costs you pay after meeting your deductible.

- Out-of-pocket maximum: This is the maximum amount you’ll pay out-of-pocket in a year. Once you reach this limit, your insurance covers 100% of your eligible expenses.

- Network of providers: Ensure your preferred doctors and hospitals are in your plan’s network. Using out-of-network providers can significantly increase your costs.

- Prescription drug coverage: Review the formulary (list of covered medications) and associated costs.

Finding the Right Plan:

Choosing the right health insurance plan is a personal decision. Carefully weigh the pros and cons of HDHPs and LDHPs, considering your individual circumstances and financial situation. Don’t hesitate to utilize online resources and compare plans. For personalized guidance in Waukesha County, www.waukeshahealthinsurance.com can provide expert advice and help you find the best plan for your needs. Remember, understanding your options is the first step toward securing affordable and effective healthcare coverage. Take your time, ask questions, and make a choice that aligns with your long-term health and financial well-being. Don’t underestimate the value of professional guidance; seeking help from an experienced insurance broker can save you time, money, and stress. Contact www.waukeshahealthinsurance.com today to begin your journey towards finding the perfect health insurance plan.