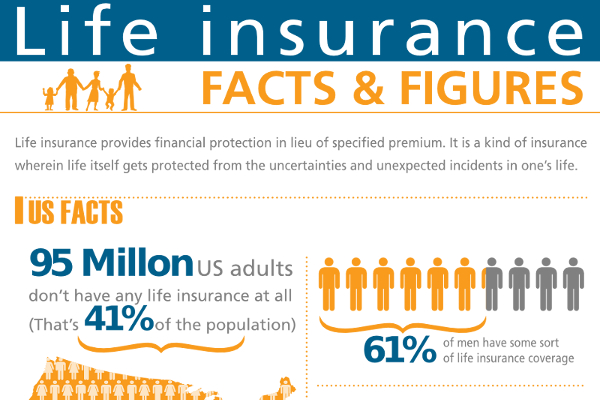

Failing to reevaluate your wants can mean that you turn out to be underinsured- something that many American households are facing, with a median insurance gap of almost $320,000.

These are essentially the most movements that wants to trigger a reevaluation:

1. Marriage and Divorce

If your spouse will rely upon your revenue for his or her source average of dwelling, you would be able to also need to building up your insurance coverage to satisfy their rates and pay off any large money owed like your mortgage.

You and your spouse will need to take some time to take into accout your lifestyles insurance expectations according with your source price wide variety. If either of you have already got toddlers, you would be able to also need to pay attention on whether make bound to be added as a beneficiary of their lifestyles insurance policy.

While loads of us get married in their 20s, the median age for second marriage is 32.6 for ladies and 35.2 for guys. Life insurance will be different for other persons in second marriages, mainly if there are step toddlers to accept as true with. The former spouse will commonly need to be removed as a beneficiary, and youll also need to accept as true with any infant support and alimony payments.

If youre getting a divorce, you would be able to also like to review your beneficiaries and be exact that any toddlers you have together will still be appropriately supported.

2. Expecting or Adopting Children

Adding toddlers to the liked ones is frequently one of the biggest triggers for other persons who are uninsured to purchase lifestyles insurance. If you have already got a policy youll need to update your insurance.

Usually, youll need to building up your cover, holding the fiscal long-term of your toddlers. This will be exact that their dwelling and education rates can be covered if you go on concurrently theyre still dependent on you.

3. A New House or Job

When you change jobs, you would be able to also discover that your new employer is maybe presenting more or loads less insurance than your final employer. This can mean that you either need to purchase supplemental coverage or scale down your source lifestyles insurance.

If your new process contains an increased salary, you would be able to also additionally like to building up your lifestyles insurance coverage. And if you purchase a new house, youll commonly like to reevaluate your lifestyles insurance to cover the mortgage.

This will prevent your spouse or toddlers from needing to promote the house in the occasion that they not have your revenue available.

4. Retirement

If your employer is providing you with lifestyles insurance, youll need to update your coverage when youre able to retire. If you have already got whole lifestyles insurance, this could in general support you cover the worth of retirement.

If youre worried about your percentages of getting insured, you would be able to also additionally have a look at lifestyles insurance no medical exam. These policies will in general cost more, nonetheless it, as the insurer is taking on more risk.

5. Annually

Reviewing your lifestyles insurance doesnt need to take decades. Mark a day on your calendar once a year to have a look at your situation and make any critical modifications.

You can also discover that movements you hadnt thought about (a bit like adult toddlers growing independent or going to university) can mean that you not need as loads insurance.

Tags

Guide